From the Harvard Business Review

By Amar Bhide

Of the hundreds of thousands of business ventures that entrepreneurs launch every year, many never get off the ground. Others fizzle after spectacular rocket starts.

A six-year-old condiment company has attracted loyal customers but has achieved less than $500,000 in sales. The company’s gross margins can’t cover its overhead or provide adequate incomes for the founder and the family members who participate in the business. Additional growth will require a huge capital infusion, but investors and potential buyers aren’t keen on small, marginally profitable ventures, and the family has exhausted its resources.

Another young company, profitable and growing rapidly, imports novelty products from the Far East and sells them to large U.S. chain stores. The founder, who has a paper net worth of several million dollars, has been nominated for entrepreneur-of-the-year awards. But the company’s spectacular growth has forced him to reinvest most of his profits to finance the business’s growing inventories and receivables. Furthermore, the company’s profitability has attracted competitors and tempted customers to deal directly with the Asian suppliers. If the founder doesn’t do something soon, the business will evaporate.

Like most entrepreneurs, the condiment maker and the novelty importer get plenty of confusing counsel: Diversify your product line. Stick to your knitting. Raise capital by selling equity. Don’t risk losing control just because things are bad. Delegate. Act decisively. Hire a professional manager. Watch your fixed costs.

Why all the conflicting advice? Because the range of options—and problems—that founders of young businesses confront is vast. The manager of a mature company might ask, What business are we in? or How can we exploit our core competencies? Entrepreneurs must continually ask themselves what business they want to be in and what capabilities they would like to develop. Similarly, the organizational weaknesses and imperfections that entrepreneurs confront every day would cause the managers of a mature company to panic. Many young enterprises simultaneously lack coherent strategies, competitive strengths, talented employees, adequate controls, and clear reporting relationships.

The problems entrepreneurs confront every day would overwhelm most managers.

The entrepreneur can tackle only one or two opportunities and problems at a time. Therefore, just as a parent should focus more on a toddler’s motor skills than on his or her social skills, the entrepreneur must distinguish critical issues from normal growing pains.

Entrepreneurs cannot expect the sort of guidance and comfort that an authoritative child-rearing book can offer parents. Human beings pass through physiological and psychological stages in a more or less predetermined order, but companies do not share a developmental path. Microsoft, Lotus, WordPerfect, and Intuit, although competing in the same industry, did not evolve in the same way. Each of those companies has its own story to tell about the development of strategy and organizational structures and about the evolution of the founder’s role in the enterprise.

Every company has its own story to tell about the development of systems and strategy.

The options that are appropriate for one entrepreneurial venture may be completely inappropriate for another. Entrepreneurs must make a bewildering number of decisions, and they must make the decisions that are right for them. The framework I present here and the accompanying rules of thumb will help entrepreneurs analyze the situations in which they find themselves, establish priorities among the opportunities and problems they face, and make rational decisions about the future. This framework, which is based on my observation of several hundred start-up ventures over eight years, doesn’t prescribe answers. Instead, it helps entrepreneurs pose useful questions, identify important issues, and evaluate solutions. The framework applies whether the enterprise is a small printing shop trying to stay in business or a catalog retailer seeking hundreds of millions of dollars in sales. And it works at almost any point in a venture’s evolution. Entrepreneurs should use the framework to evaluate their companies’ position and trajectory often—not just when problems appear.

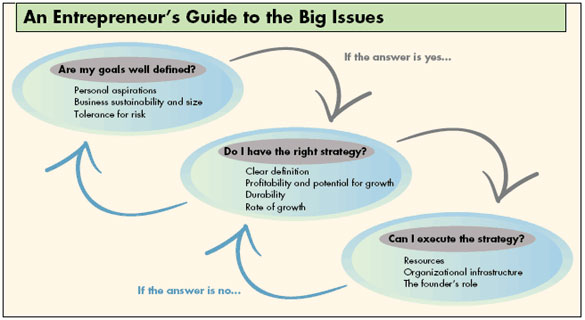

The framework consists of a three-step sequence of questions. The first step clarifies entrepreneurs’ current goals, the second evaluates their strategies for attaining those goals, and the third helps them assess their capacity to execute their strategies. The hierarchical organization of the questions requires entrepreneurs to confront the basic, big-picture issues before they think about refinements and details. (See the exhibit “An Entrepreneur’s Guide to the Big Issues.”) This approach does not assume that all companies—or all entrepreneurs—develop in the same way, so it does not prescribe a one-size-fits-all methodology for success.

An Entrepreneur’s Guide to the Big Issues

An entrepreneur’s personal and business goals are inextricably linked. Whereas the manager of a public company has a fiduciary responsibility to maximize value for shareholders, entrepreneurs build their businesses to fulfill personal goals and, if necessary, seek investors with similar goals.

Before they can set goals for a business, entrepreneurs must be explicit about their personal goals. And they must periodically ask themselves if those goals have changed. Many entrepreneurs say that they are launching their businesses to achieve independence and control their destiny, but those goals are too vague. If they stop and think about it, most entrepreneurs can identify goals that are more specific. For example, they may want an outlet for artistic talent, a chance to experiment with new technology, a flexible lifestyle, the rush that comes from rapid growth, or the immortality of building an institution that embodies their deeply held values. Financially, some entrepreneurs are looking for quick profits, some want to generate a satisfactory cash flow, and others seek capital gains from building and selling a company. Some entrepreneurs who want to build sustainable institutions do not consider personal financial returns a high priority. They may refuse acquisition proposals regardless of the price or sell equity cheaply to employees to secure their loyalty to the institution.

Only when entrepreneurs can say what they want personally from their businesses does it make sense for them to ask the following three questions:

What kind of enterprise do I need to build?

Long-term sustainability does not concern entrepreneurs looking for quick profits from in-and-out deals. Similarly, so-called lifestyle entrepreneurs, who are interested only in generating enough of a cash flow to maintain a certain way of life, do not need to build businesses that could survive without them. But sustainability—or the perception thereof—matters greatly to entrepreneurs who hope to sell their businesses eventually. Sustainability is even more important for entrepreneurs who want to build an institution that is capable of renewing itself through changing generations of technology, employees, and customers.

Entrepreneurs’ personal goals should also determine the target size of the businesses they launch. A lifestyle entrepreneur’s venture needn’t grow very large. In fact, a business that becomes too big might prevent the founder from enjoying life or remaining personally involved in all aspects of the work. In contrast, entrepreneurs seeking capital gains must build companies large enough to support an infrastructure that will not require their day-to-day intervention.

What risks and sacrifices does such an enterprise demand?

Building a sustainable business—that is, one whose principal productive asset is not just the founder’s skills, contacts, and efforts—often entails making risky long-term bets. Unlike a solo consulting practice—which generates cash from the start—durable ventures, such as companies that produce branded consumer goods, need continued investment to build sustainable advantages. For instance, entrepreneurs may have to advertise to build a brand name. To pay for ad campaigns, they may have to reinvest profits, accept equity partners, or personally guarantee debt. To build depth in their organizations, entrepreneurs may have to trust inexperienced employees to make crucial decisions. Furthermore, many years may pass before any payoff materializes—if it materializes at all. Sustained risk taking can be stressful. As one entrepreneur observes, “When you start, you just do it, like the Nike ad says. You are naïve because you haven’t made your mistakes yet. Then you learn about all the things that can go wrong. And because your equity now has value, you feel you have a lot more to lose.”

Entrepreneurs who operate small-scale, or lifestyle, ventures face different risks and stresses. Talented people usually avoid companies that offer no stock options and only limited opportunities for personal growth, so the entrepreneur’s long hours may never end. Because personal franchises are difficult to sell and often require the owner’s daily presence, founders may become locked into their businesses. They may face financial distress if they become sick or just burn out. “I’m always running, running, running,” complains one entrepreneur, whose business earns him half a million dollars per year. “I work 14-hour days, and I can’t remember the last time I took a vacation. I would like to sell the business, but who wants to buy a company with no infrastructure or employees?”

Can I accept those risks and sacrifices?

Entrepreneurs must reconcile what they want with what they are willing to risk. Consider Joseph Alsop, co-founder and president of Progress Software Corporation. When Alsop launched the company in 1981, he was in his mid-thirties, with a wife and three children. With that responsibility, he says, he didn’t want to take the risks necessary to build a multi-billion-dollar corporation like Microsoft, but he and his partners were willing to assume the risks required to build something more than a personal service business. Consequently, they picked a market niche that was large enough to let them build a sustainable company but not so large that it would attract the industry’s giants. They worked for two years without salaries and invested their personal savings. In ten years, they had built Progress into a $200 million publicly held company.

To set meaningful goals, entrepreneurs must reconcile what they want with what they are willing to risk.

Entrepreneurs would do well to follow Alsop’s example by thinking explicitly about what they are and are not willing to risk. If entrepreneurs find that their businesses—even if very successful—won’t satisfy them personally, or if they discover that achieving their personal goals requires them to take more risks and make more sacrifices than they are willing to, they need to reset their goals. When entrepreneurs have aligned their personal and their business goals, they must then make sure that they have the right strategy.

Setting Strategy: How Will I Get There?Many entrepreneurs start businesses to seize short-term opportunities without thinking about long-term strategy. Successful entrepreneurs, however, soon make the transition from a tactical to a strategic orientation so that they can begin to build crucial capabilities and resources.

Formulating a sound strategy is more basic to a young company than resolving hiring issues, designing control systems, setting reporting relationships, or defining the founder’s role. Ventures based on a good strategy can survive confusion and poor leadership, but sophisticated control systems and organizational structures cannot compensate for an unsound strategy. Entrepreneurs should periodically put their strategies to the following four tests:

Is the strategy well defined?

A company’s strategy will fail all other tests if it doesn’t provide a clear direction for the enterprise. Even solo entrepreneurs can benefit from a defined strategy. For example, deal makers who specialize in particular industries or types of transactions often have better access to potential deals than generalists do. Similarly, independent consultants can charge higher fees if they have a reputation for expertise in a particular area.

An entrepreneur who wants to build a sustainable company must formulate a bolder and more explicit strategy. The strategy should integrate the entrepreneur’s aspirations with specific long-term policies about the needs the company will serve, its geographic reach, its technological capabilities, and other strategic considerations. To help attract people and resources, the strategy must embody the entrepreneur’s vision of where the company is going instead of where it is. The strategy must also provide a framework for making the decisions and setting the policies that will take the company there.

A new company’s strategy must embody the founder’s vision of where the company is going, not where it is.

The strategy articulated by the founders of Sun Microsystems, for instance, helped them make smart decisions as they developed the company. From the outset, they decided that Sun would forgo the niche-market strategy commonly used by Silicon Valley start-ups. Instead, they elected to compete with industry leaders IBM and Digital by building and marketing a general-purpose workstation. That strategy, recalls cofounder and former president Vinod Khosla, made Sun’s product-development choices obvious. “We wouldn’t develop any applications software,” he explains. This strategy also dictated that Sun assume the risk of building a direct sales force and providing its own field support—just like its much larger competitors. “The Moon or Bust was our motto,” Khosla says. The founders’ bold vision helped attract premier venture-capital firms and gave Sun extraordinary visibility within its industry.

To be useful, strategy statements should be concise and easily understood by key constituents such as employees, investors, and customers. They must also preclude activities and investments that, although they seem attractive, would deplete the company’s resources. A strategy that is so broadly stated that it permits a company to do anything is tantamount to no strategy at all. For instance, claiming to be in the leisure and entertainment business does not preclude a tent manufacturer from operating casinos or making films. Defining the venture as a high-performance outdoor-gear company provides a much more useful focus.

Can the strategy generate sufficient profits and growth?

Once entrepreneurs have formulated clear strategies, they must determine whether those strategies will allow the ventures to be profitable and to grow to a desirable size. The failure to earn satisfactory returns should prompt entrepreneurs to ask tough questions: What’s the source, if any, of our competitive edge? Are our offerings really better than our competitors’? If they are, does the premium we can charge justify the additional costs we incur, and can we move enough volume at higher prices to cover our fixed costs? If we are in a commodity business, are our costs lower than our competitors’? Disappointing growth should also raise concerns: Is the market large enough? Do diseconomies of scale make profitable growth impossible?

No amount of hard work can turn a kitten into a lion. When a new venture is faltering, entrepreneurs must address basic economic issues. For instance, many people are attracted to personal service businesses, such as laundries and tax-preparation services, because they can start and operate those businesses just by working hard. They don’t have to worry about confronting large competitors, raising a lot of capital, or developing proprietary technology. But the factors that make it easy for entrepreneurs to launch such businesses often prevent them from attaining their long-term goals. Businesses based on an entrepreneur’s willingness to work hard usually confront other equally determined competitors. Furthermore, it is difficult to make such companies large enough to support employees and infrastructure. Besides, if employees can do what the founder does, they have little incentive to stay with the venture. Founders of such companies often cannot have the lifestyle they want, no matter how talented they are. With no way to leverage their skills, they can eat only what they kill.

Entrepreneurs who are stuck in ventures that are unprofitable and cannot grow satisfactorily must take radical action. They must find a new industry or develop innovative economies of scale or scope in their existing fields. Rebecca Matthias, for example, started Mothers Work in 1982 to sell maternity clothing to professional women by mail order. Mail-order businesses are easy to start, but with tens of thousands of catalogs vying for consumers’ attention, low response rates usually lead to low profitability—a reality that Matthias confronted after three years in the business. In 1985, she borrowed $150,000 to open the first retail store specializing in maternity clothes for working women. By 1994, Mothers Work was operating 175 stores generating about $59 million in revenues.

One alternative to radical action is to stick with the failing venture and hope for the big order that’s just around the corner or the greater fool who will buy the business. Both hopes are usually futile. It’s best to walk away.

Is the strategy sustainable?

The next issue entrepreneurs must confront is whether their strategies can serve the enterprise over the long term. The issue of sustainability is especially significant for entrepreneurs who have been riding the wave of a new technology, a regulatory change, or any other change—exogenous to the business—that creates situations in which supply cannot keep up with demand. Entrepreneurs who catch a wave can prosper at the outset just because the trend is on their side; they are competing not with one another but with outmoded players. But what happens when the wave crests? As market imbalances disappear, so do many of the erstwhile high fliers who had never developed distinctive capabilities or established defensible competitive positions. Wave riders must anticipate market saturation, intensifying competition, and the next wave. They have to abandon the me-too approach in favor of a new, more durable business model. Or they may be able to sell their high-growth businesses for handsome prices in spite of the dubious long-term prospects.

Consider Edward Rosen, who cofounded Vydec in 1972. The company developed one of the first stand-alone word processors, and as the market for the machines exploded, Vydec rocketed to $90 million in revenues in its sixth year, with nearly 1,000 employees in the United States and Europe. But Rosen and his partner could see that the days of stand-alone word processors were numbered. They happily accepted an offer from Exxon to buy the company for more than $100 million.

Such forward thinking is an exception. Entrepreneurs in rapidly growing companies often don’t consider exit strategies seriously. Encouraged by short-term success, they continue to reinvest profits in unsustainable businesses until all they have left is memories of better days.

Entrepreneurs who start ventures not by catching a wave but by creating their own wave face a different set of challenges in crafting a sustainable strategy. They must build on their initial strength by developing multiple strengths. Brand-new ventures usually cannot afford to innovate on every front. Few start-ups, for example, can expect to attract the resources needed to market a revolutionary product that requires radical advances in technology, a new manufacturing process, and new distribution channels. Cash-strapped entrepreneurs usually focus first on building and exploiting a few sources of uniqueness and use standard, readily available elements in the rest of the business. Michael Dell, the founder of Dell Computer, for example, made low price an option for personal computer buyers by assembling standard components in a college dormitory room and selling by mail order without frills or much sales support.

Strategies for taking the hill, however, won’t necessarily hold it. A model based on one or two strengths becomes obsolete as success begets imitation. For instance, competitors can easily knock off an entrepreneur’s innovative product. But they will find it much more difficult to replicate systems that incorporate many distinct and complementary capabilities. A business with an attractive product line, well-integrated manufacturing and logistics, close relationships with distributors, a culture of responsiveness to customers, and the capability to produce a continuing stream of product innovations is not easy to copy.

It’s easy to knock off an innovative product, but an innovative business system is much harder to replicate.

Entrepreneurs who build desirable franchises must quickly find ways to broaden their competitive capabilities. For example, software start-up Intuit’s first product, Quicken, had more attractive features and was easier to use than other personal-finance software programs. Intuit realized, however, that competitors could also make their products easy to use, so the company took advantage of its early lead to invest in a variety of strengths. Intuit enhanced its position with distributors by introducing a family of products for small businesses, including QuickBooks, an accounting program. It brought sophisticated marketing techniques to an industry that “viewed customer calls as interruptions to the sacred art of programming,” according to the company’s founder and chairman, Scott Cook. It established a superior product-design process with multifunctional teams that included marketing and technical support. And Intuit invested heavily to provide customers with outstanding technical support for free.

Are my goals for growth too conservative or too aggressive?

After defining or redefining the business and verifying its basic soundness, an entrepreneur should determine whether plans for its growth are appropriate. Different enterprises can and should grow at different rates. Setting the right pace is as important to a young business as it is to a novice bicyclist. For either one, too fast or too slow can lead to a fall. The optimal growth rate for a fledgling enterprise is a function of many interdependent factors. (See the insert “Finding the Right Growth Rate.”)

Finding the Right Growth Rate

Finding the optimal growth rate for a new enterprise is a difficult and critical task. To set the right pace, entrepreneurs must ...

Executing the Strategy: Can I Do It?The third question entrepreneurs must ask themselves may be the hardest to answer because it requires the most candid self-examination: Can I execute the strategy? Great ideas don’t guarantee great performance. Many young companies fail because the entrepreneur can’t execute the strategy; for instance, the venture may run out of cash, or the entrepreneur may be unable to generate sales or fill orders. Entrepreneurs must examine three areas—resources, organizational capabilities, and their personal roles—to evaluate their ability to carry out their strategies.

Do I have the right resources and relationships?

The lack of talented employees is often the first obstacle to the successful implementation of a strategy. During the start-up phase, many ventures cannot attract top-notch employees, so the founders perform most of the crucial tasks themselves and recruit whomever they can to help out. After that initial period, entrepreneurs can and should be ambitious in seeking new talent, especially if they want their businesses to grow quickly. Entrepreneurs who hope that they can turn underqualified and inexperienced employees into star performers eventually reach the conclusion, along with Intuit founder Cook, that “you can’t coach height.” Moreover, after a venture establishes even a short track record, it can attract a much higher caliber of employee.

Entrepreneurs who hope to turn underqualified employees into star performers are almost always disappointed.

In determining how to upgrade the workforce, entrepreneurs must address many complex and sensitive issues: Should I recruit individuals for specific slots or, as is commonly the case in talent-starved organizations, should I create positions for promising candidates? Are the recruits going to manage or replace existing employees? How extensive should the replacements be? Should the replacement process be gradual or quick? Should I, with my personal attachment to the business, make termination decisions myself or should I bring in outsiders?

A young venture needs more than internal resources. Entrepreneurs must also consider their customers and sources of capital. Ventures often start with the customers they can attract the most quickly, which may not be the customers the company eventually needs. Similarly, entrepreneurs who begin by bootstrapping, using money from friends and family or loans from local banks, must often find richer sources of capital to build sustainable businesses.

For a new venture to survive, some resources that initially are external may have to become internal. Many start-ups operate at first as virtual enterprises because the founders cannot afford to produce in-house and hire employees, and because they value flexibility. But the flexibility that comes from owning few resources is a double-edged sword. Just as a young company is free to stop placing orders, suppliers can stop filling them. Furthermore, a company with no assets signals to customers and potential investors that the entrepreneur may not be committed for the long haul. A business with no employees and hard assets may also be difficult to sell, because potential buyers will probably worry that the company will vanish when the founder departs. To build a durable company, an entrepreneur may have to consider integrating vertically or replacing subcontractors with full-time employees.

How strong is the organization?

An organization’s capacity to execute its strategy depends on its “hard” infrastructure—its organizational structure and systems—and on its “soft” infrastructure—its culture and norms.

The hard infrastructure an entrepreneurial company needs depends on its goals and strategies. (See the insert “Investing in Organizational Infrastructure.”) Some entrepreneurs want to build geographically dispersed businesses, realize synergies by sharing resources across business units, establish first-mover advantages through rapid growth, and eventually go public. They must invest more in organizational infrastructure than their counterparts who want to build simple, single-location businesses at a cautious pace.

Investing in Organizational Infrastructure

Few entrepreneurs start out with both a well-defined strategy and a plan for developing an organization that can achieve ...

A venture’s growth rate provides an important clue to whether the entrepreneur has invested too much or too little in the company’s structure and systems. If performance is sluggish—if, for example, growth lags behind expectations and new products are late—excessive rules and controls may be stifling employees. If, in contrast, the business is growing rapidly and gaining share, inadequate reporting mechanisms and controls are a more likely concern. When a new venture is growing at a fast pace, entrepreneurs must simultaneously give new employees considerable responsibility and monitor their finances very closely. Companies like Block-buster Video cope by giving frontline employees all the operating autonomy they can handle while maintaining tight, centralized financial controls.

An evolving organization’s culture also has a profound influence on how well it can execute its strategy. Culture determines the personalities and temperaments of the workforce; lone wolves are unlikely to want to work in a consensual organization, whereas shy introverts may avoid rowdy outfits. Culture fills in the gaps that an organization’s written rules do not anticipate. Culture determines the degree to which individual employees and organizational units compete and cooperate, and how they treat customers. More than any other factor, culture determines whether an organization can cope with the crises and discontinuities of growth.

Unlike organizational structures and systems, which entrepreneurs often copy from other companies, culture must be custom built. As many software makers have found, for instance, a laid-back organization can’t compete well against Microsoft. The rambunctiousness of a start-up trading operation may scare away the conservative clients the venture wants to attract. A culture that fits a company’s strategy, however, can lead to spectacular performance. Physician Sales & Service (PSS), a medical-products distribution company, has grown from $13 million in sales in 1987 to nearly $500 million in 1995, from 5 branches in Florida to 56 branches covering every state in the continental United States, and from 120 employees to 1,800. Like other rapidly growing companies, PSS has tight financial controls. But, venture capitalist Thomas Dickerson says, “PSS would be just another efficiently managed distribution company if it didn’t have a corporate culture that is obsessed with meeting customers’ needs and maintaining a meritocracy. PSS employees are motivated by the culture to provide unmatched customer service.”

When entrepreneurs neglect to articulate organizational norms and instead hire employees mainly for their technical skills and credentials, their organizations develop a culture by chance rather than by design. The personalities and values of the first wave of employees shape a culture that may not serve the founders’ goals and strategies. Once a culture is established, it is difficult to change.

When entrepreneurs don’t stop to think about culture, their companies develop one by chance rather than by design.

Can I play my role?

Entrepreneurs who aspire to operate small enterprises in which they perform all crucial tasks never have to change their roles. In personal service companies, for instance, the founding partners often perform client work from the time they start the company until they retire. Transforming a fledgling enterprise into an entity capable of an independent existence, however, requires founders to undertake new roles.

Founders cannot build self-sustaining organizations simply by “letting go.” Before entrepreneurs have the option of doing less, they first must do much more. If the business model is not sustainable, they must create a new one. To secure the resources demanded by an ambitious strategy, they must manage the perceptions of the resource providers: potential customers, employees, and investors. To build an enterprise that will be able to function without them, entrepreneurs must design the organization’s structure and systems and mold its culture and character.

While they are sketching out an expansive view of the future, entrepreneurs also have to manage as if the company were on the verge of going under, keeping a firm grip on expenses and monitoring performance. They have to inspire and coach employees while dealing with the unpleasantness of firing those who will not be able to grow with the company. Bill Nussey, cofounder of the software maker Da Vinci Systems Corporation, recalls that firing employees who had “struggled and cried and sacrificed with the company” was the hardest thing he ever had to do.

Few successful entrepreneurs ever come to play a purely visionary role in their organizations. They remain deeply engaged in what Abraham Zaleznik, the Konosuke Matsushita Professor of Leadership Emeritus at the Harvard Business School, calls the “real work” of their enterprises. Marvin Bower, the founding partner of McKinsey & Company, continued to negotiate and direct studies for clients while leading the firm through a considerable expansion of its size and geographic reach. Bill Gates, co-founder and CEO of multibillion-dollar software powerhouse Microsoft, reportedly still reviews the code that programmers write.

But founders’ roles must change. Gates no longer writes programs. Michael Roberts, an expert on entrepreneurship, suggests that an entrepreneur’s role should evolve from doing the work, to teaching others how to do it, to prescribing desired results, and eventually to managing the overall context in which the work is done. One entrepreneur speaks of changing from quarterback to coach. Whatever the metaphor, the idea is that leaders seek ever increasing impact from what they do. They achieve this by, for example, focusing more on formulating marketing strategies than on selling; negotiating and reviewing budgets rather than directly supervising work; designing incentive plans rather than setting the compensation of individual employees; negotiating the acquisitions of companies instead of the cost of office supplies; and developing a common purpose and organizational norms rather than moving a product out the door.

In evaluating their personal roles, therefore, entrepreneurs should ask themselves whether they continually experiment with new jobs and responsibilities. Founders who simply spend more hours performing the same tasks and making the same decisions as the business grows end up hindering growth. They should ask themselves whether they have acquired any new skills recently. An entrepreneur who is an engineer, for example, might master financial analysis. If founders can’t point to new skills, they are probably in a rut and their roles aren’t evolving.

Entrepreneurs must ask themselves whether they actually want to change and learn. People who enjoy taking on new challenges and acquiring new skills—Bill Gates, again—can lead a venture from the start-up stage to market dominance. But some people, such as H. Wayne Huizenga, the moving spirit behind Waste Management and Blockbuster Video, are much happier moving on to get other ventures off the ground. Entrepreneurs have a responsibility to themselves and to the people who depend on them to understand what fulfills and frustrates them personally.

Many great enterprises spring from modest, improvised beginnings. William Hewlett and David Packard tried to craft a bowling alley foot-fault indicator and a harmonica tuner before developing their first successful product, an audio oscillator. Wal-Mart Stores’ founder, Sam Walton, started by buying what he called a “real dog” of a franchised variety store in Newport, Arkansas, because his wife wanted to live in a small town. Speedy response and trial and error were more important to those companies at the start-up stage than foresight and planning. But pure improvisation—or luck—rarely yields long-term success. Hewlett-Packard might still be an obscure outfit if its founders had not eventually made conscious decisions about product lines, technological capabilities, debt policies, and organizational norms.

Entrepreneurs, with their powerful bias for action, often avoid thinking about the big issues of goals, strategies, and capabilities. They must, sooner or later, consciously structure such inquiry into their companies and their lives. Lasting success requires entrepreneurs to keep asking tough questions about where they want to go and whether the track they are on will take them there.

Amar Bhidé is the Thomas Schmidheiny Professor at the Fletcher School at Tufts University in Somerville and Medford, Massachusetts, and a visiting professor at Harvard Business School (HBS) in Boston, Massachusetts. He is a member of the Council on Foreign Relations, a founding member of the Center on Capitalism and Society, and the author of “A Call for Judgment: Sensible Finance for a Dynamic Economy” (Oxford, 2010). A former senior engagement manager at McKinsey & Company and proprietary trader at E.F. Hutton, Bhidé also served on the staff of the Brady Commission, which investigated the 1987 stock market crash.

© 2021 Money Matters | ALL RIGHTS RESERVED.

DESIGNED BY TIMGREGG.COM